2025 – The Year of Artificial Intelligence (AI).

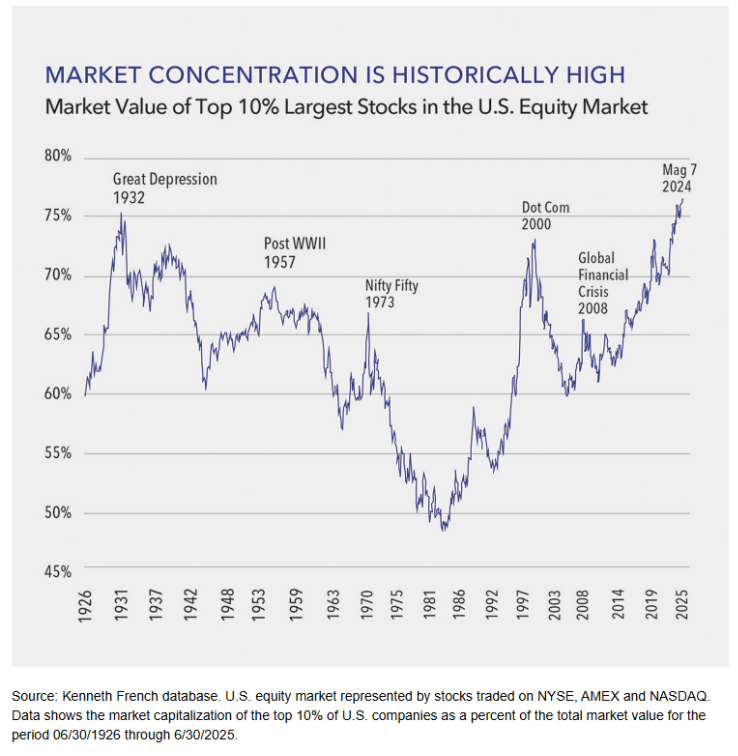

Market concentration hits all-time highs – The market’s focus on a handful of companies perceived as AI winners has created a top-heavy market ripe for disruption.

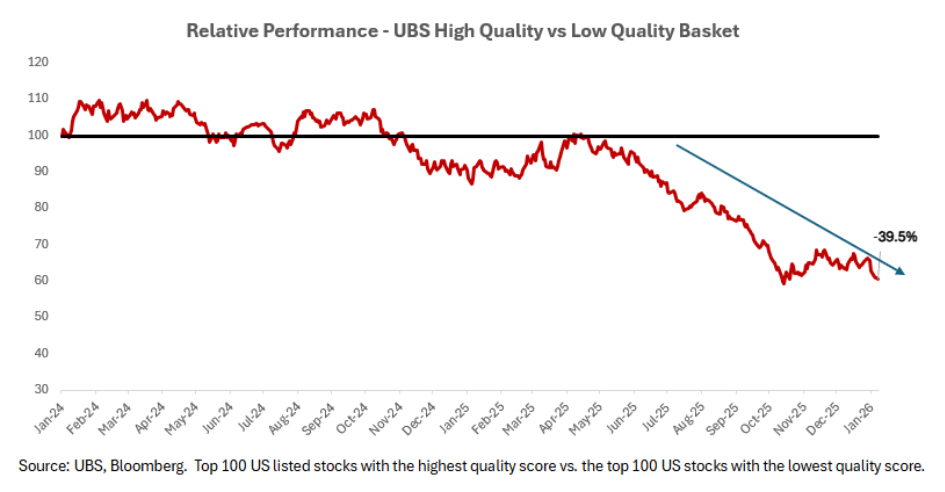

Quality is on sale – Quality companies underperformed by a wide margin in the second half, giving investors willing to look outside of yesterday’s winners a golden opportunity.

Focus on downside risk – We continue to focus on the long-term and invest in companies with strong competitive advantages that will provide downside protection.

While the fourth quarter brought a brief reprieve, or at least a shift in the perceived AI winners, 2025 will likely be remembered as an all-or-nothing AI driven market that pushed market concentration to record levels. Since the release of ChatGPT in late 2022, AI mania has gripped the markets and investors quickly anointed a handful of companies as the winners, resulting in a small number of firms driving market returns. Meanwhile, many companies, and even entire industries, have been labeled as AI losers, resulting in notable declines in their share prices, creating a golden opportunity to purchase some very high-quality companies at attractive valuations.

Market concentration hits a new high.

While 2025 stood out in several respects, short-term market performance is often driven by investor sentiment, especially when a particular trend captures investors’ attention and money managers feel pressure to follow or risk being left behind. In many cases, these trends fade quickly, and investors return to fundamentals such as earnings growth. Occasionally, an extreme example prompts a massive boom-and-bust cycle, as witnessed during the late 1990’s internet bubble, when traditional metrics such as P/E ratios were replaced with novel measures such as ‘eyeballs’. One company simply renamed itself Internet.com and saw its share price jump nearly 60 per cent. The inevitable outcome was a massive correction that saw many previous high-flyers fall into bankruptcy.

While not quite as extreme, in recent years the majority of market gains have come from just a handful of companies known as the “Magnificent 7”: Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla. Market concentration recently hit a record high, with Information Technology and Communication Services (led by Alphabet and Meta) gaining sector weight at the expense of most other sectors. Over the past two years, the AI-frenzy has amplified this trend, with investors chasing a narrow range of companies and neglecting large swaths of the market.

Market concentration at these levels introduces potential risk, as any loss of confidence in these companies could incite a broader market pullback. However, investors considering the broader market are afforded opportunities to identify high quality companies often overlooked due to exclusion from the AI trend. It’s these companies we focus on and believe will offer downside protection in the event of a market reversal and subsequent return to a more normalized market breadth.

Quality is on sale.

Rarely has there been a more opportune time to buy quality companies given the dramatic underperformance over the last 12 months, one of the worst runs in history.

Over the last couple of years, quality-focused investing has become exceedingly difficult as markets chase the AI trade. Investors have disregarded a group of companies that includes high-barrier industries such as the credit card networks (Visa, Mastercard), waste collection (Waste Connections, Waste Management, Republic Services), industrial gases (Linde, Air Products, Air Liquide), and rating agencies (Moody’s, S&P Global).

Each of these industries includes companies with characteristics we seek in our investments. Waste Connections, a long-time holding in our Canadian Equity Fund, is one of three major US waste companies, which together control roughly 50 per cent of the market. Since it’s close to impossible to get a new landfill approved (most approvals involve the expansion of existing sites), we don’t expect a new entrant to emerge anytime soon, especially not one owning the most valuable part of the waste chain: the landfill. This pattern of market dominance extends to our holdings in the credit rating space. Moody’s and S&P Global, both held in our Global Equity Fund, together account for more than 80 per cent of the worldwide debt rating market. This highly regulated sector makes it nearly impossible for new entrants to take meaningful share, creating a near duopoly. Furthermore, since it’s standard practice for at least two agencies to rate any new bond issuance, Moody’s and S&P often evaluate the same debt. This removes the incentive to compete on price, further protecting their margins.

As investors chase the AI theme, companies with consistent earnings growth, low leverage, and, most importantly, proven longevity are being overlooked. While it’s difficult to predict what Tesla will look like in 10, or even 5 years, there’s little doubt about the future of these holdings. Waste Connections will be doing exactly what it’s done for the past 30 years: collecting and disposing of waste. Similarly, Moody’s and S&P will continue to provide global debt rating services, just as they have for more than a century.

Who will win the AI race?

History suggests that the early declarations of winners and losers are often premature as we saw during both the PC boom of the 1980s and the internet boom of the 1990s. While history may not repeat, though it clearly rhymes, we’re already seeing that pattern play out in real time. Consider the example of Google: in as little as two years, it went from being almost universally considered one of the biggest losers in the world of AI to now being seen as the clear frontrunner.

In December 2022, shares of Alphabet (owner of Google) fell below US$85 from a recent high of over US$150. Investors were rightfully concerned that its core search business was at risk of disruption after OpenAI released its first AI chatbot, ChatGPT, to an overwhelmingly positive reception. Stories of Google issuing a “code red” ran rampant, and a wide range of experts, including the well-respected inventor of Gmail, were calling for the death of search. Things went from bad to worse a couple of months later when Google did an initial demo of its own AI chatbot and its response to a question included a factual error, leading to questions about the company’s ability to keep up in the AI race. It didn’t take long, however, for the company to prove that this initial skepticism was unfounded and the belief that search was dead was premature, at best.

Following the release of an updated version of Gemini that was well-received by users, alongside strong search revenue and usage in subsequent quarters, market sentiment toward Google began to shift positively. Over the past several months, this shift has accelerated, with Google increasingly viewed as the preferred AI investment relative to OpenAI. Investors have taken note of the company’s roughly US$140 billion in annual net income and its ownership of critical AI assets, including proprietary semiconductor chips (TPUs), a leading AI model (Gemini), and unparalleled data from its 3.5 billion users across platforms such as Search and YouTube. The result has been a dramatic reversal in Google’s share price, which is now trading just above US$325. Adding to the drama, after Google released its most up to date model in November, Gemini 3.0, to rave reviews, a leaked internal memo from OpenAI revealed that it had declared its own code red emergency, resulting in a complete reversal of roles between the two players.

Final thoughts.

Markets often project certainty, but what seems obvious today frequently looks far less so in hindsight. Even Nvidia, one of the largest beneficiaries of the AI arms race, appears less invincible as it once did. Investors are starting to question whether it can sustain its extraordinary margins, given that most of its sales come from a small number of customers funding currently unprofitable businesses where Nvidia chips account for roughly 80 per cent of costs.

While others continue to debate the unknown and speculate on the next phase of the AI trade, we remain focused on the facts and our process. By finding high-quality, SRI-focused companies with proven track records and longevity, we build resilient portfolios we can comfortably own over the long-term that offer the downside protection we seek.