.jpg)

Emotional investing is easy to fall into, but it can wreak havoc on any portfolio.

Over the last few weeks, we have had a sizable drawdown in global equity markets. While the speed and size of such drawdowns can create uneasiness for investors, it is important not to let emotions drive investment decisions when such events occur. Maintaining a long-term focus and staying invested has delivered strong compounding returns to investors. Investors who have remained invested from the start of the Global Financial Crisis in August 2007 through to August 6, 2024, have enjoyed 8.4% annualized total returns from the broad equity market. Remember this period also includes the equity market sell-off that occurred during the global pandemic as well as the recent heightened inflationary environment and central bank tightening cycle. Maintaining a long-term perspective in investing and not allowing decisions to be driven by emotional reactions to market movements is a sound investment strategy.

While market drawdowns/corrections are a normal part of investing, each one has its unique characteristics. This recent drawdown came after an extraordinarily strong start to the year. Even after this correction the global equity market has delivered a 12.7% YTD return to investors1.

There has been a fair amount of exuberance in investor sentiment this year, particularly around mega-cap tech stocks and within the technology focused Nasdaq index. Up to mid-July, the S&P 500 was up 19% YTD in USD terms, while the Nasdaq Composite index was up 24%….an extremely strong start to the year. What this tells us is that the starting point of the current drawdown was from a place of heightened optimism.

The strong start to the year naturally increases the market’s sensitivity to changes in bullish narratives, and we had more than one key spark point.

• As we are all likely aware, AI and the related hardware/infrastructure spending has been a major thematic angle for equity markets since 2023. Now investors are questioning how and when the billions of dollars being spent on AI infrastructure is going to increase corporate profitability.

• Concurrently, fears on economic weakness reemerged. The global economy is slowing, and has been for two years, but investors are now concerned it is slowing too quickly for a “soft landing”. Global economic weakness has been masked by a more resilient picture in the US, but recent weaker-than-expected economic data points in the US spooked investors (back to “pricing in” a potential recession).

• Thirdly, we had a spark of “mechanical” selling pressure adding to the already unsteady sentiment. A recent rate hike by the Bank of Japan is driving the reversal of the common “yen carry trade”. The rate hike on July 31st follows a small March hike but marks a significant shift in BoJ policy after an extended period of near zero rates. Many larger-scale investors/traders have become accustomed to borrowing cheaply in Japanese Yen and investing the proceeds in higher-yielding assets denominated in other currencies (e.g., US stocks). Last week’s interest rate hike in Japan boosted the yen significantly, forcing investors to unwind carry trades. Traders scrambled to sell higher risk, dollar-denominated assets to cover suddenly higher borrowing costs, plus FX losses and general losses in asset values as share prices dropped. Hedge funds, reliant on complex models for risk management, amplified these selling pressures.

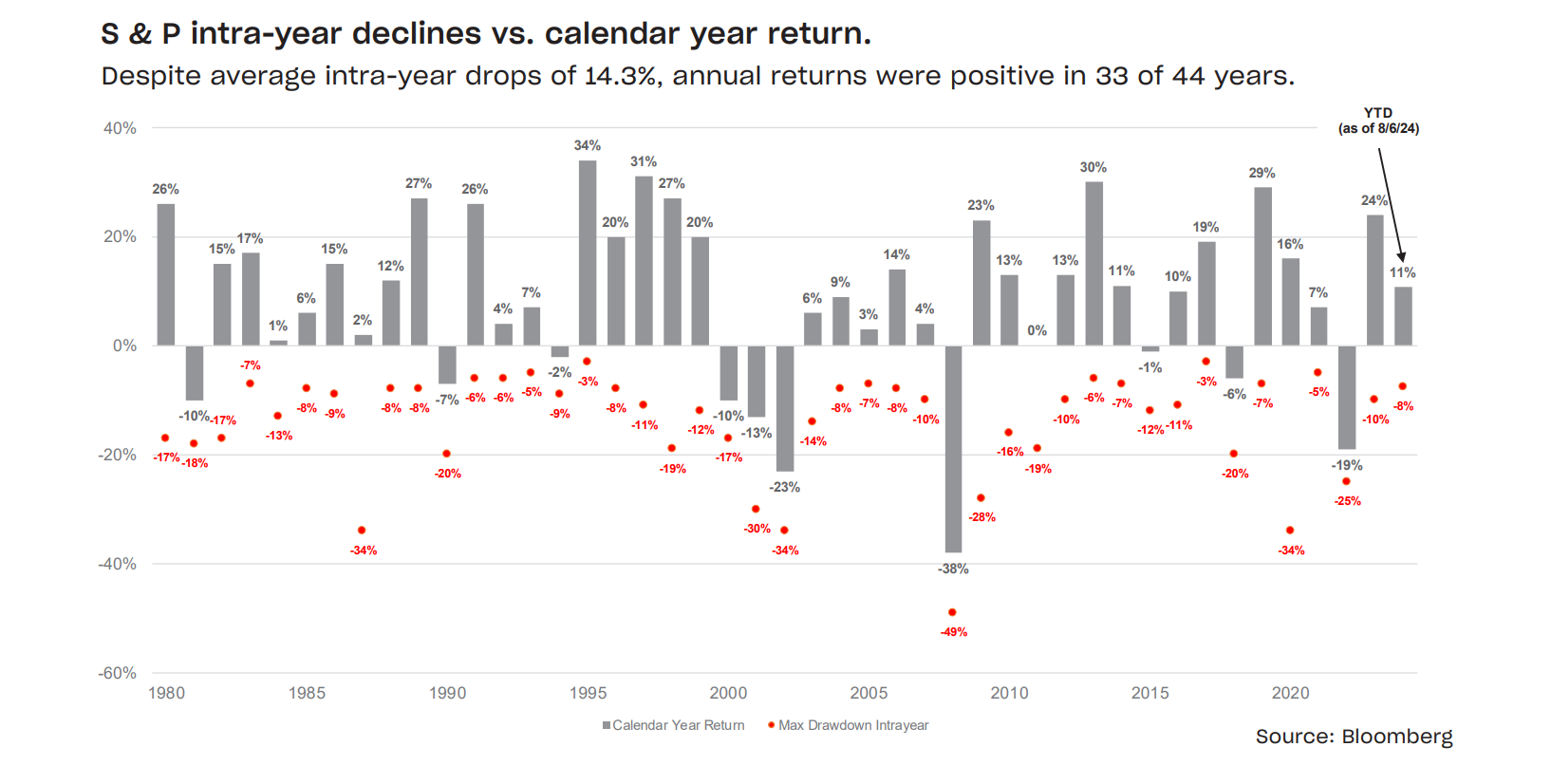

While the specifics of market corrections are unique, it is important to remember they are a natural part of investing. Corrections are scary in the moment but happen in some form every year and are particularly expected after periods of strong market performance (as we have seen YTD).

As always, we never advocate for market timing and while we do not chase or run away from markets trends, that does not mean we do not analyze and stay aware as we make investment decisions to drive long-term compounding returns for clients. In times like these, our advice for clients always falls back on our core belief in the power of staying invested despite short-term volatility. Emotional investing is easy to fall into, but it can wreak havoc on any portfolio. As the investing legend Peter Lynch has said, “Far more money has been lost by investors trying to anticipate corrections, than lost in the corrections themselves.

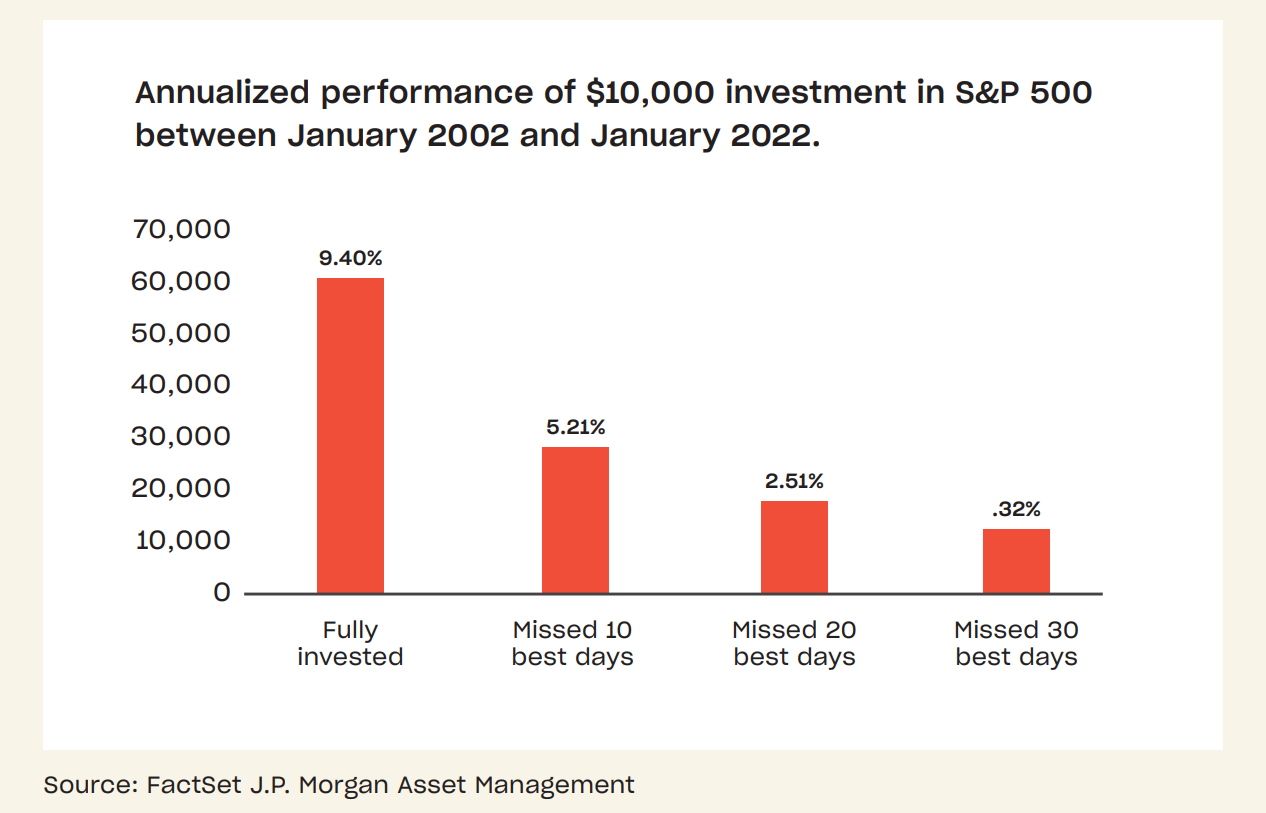

The market’s best days typically follow the largest drops, meaning panic selling can lead to missed opportunities on the upside.

"I can’t time stocks... I don’t know anybody else who can either.” – Warren Buffett

1As measured by the MSCI World Net Total Return CAD Index.

The information contained herein has been provided by Vancity Investment Management for information purposes only. It does not constitute financial, tax or legal advice. Always consult with your Portfolio Manager or a qualified advisor prior to making any investment decision. The information has been obtained from sources believed to be reliable, however we cannot guarantee that it is accurate or complete. Any reference to past returns, charts, or graphs are for illustrative purposes only and are not indicative of future performance.